Ares Capital is not a REIT—it is the largest publicly traded business development company (BDC) in the United States, with a $22 billion portfolio of directly originated, senior-secured loans to middle-market companies. For two decades, ARCC has been the gold standard in the BDC space, delivering steady net investment income, a regularly rising dividend, and sector-leading credit performance. Yet the question for income investors today is how the Federal Reserve’s rate-cutting cycle, which has brought the fed funds rate from 5.50% down to 3.75%–4.00%, will affect its floating-rate-heavy loan book and the safety of its 9% dividend yield. We analyze Ares Capital’s latest quarterly results, its balance-sheet structure, and the critical relationship between base rates, debt cost, and dividend coverage.

Latest Financial Performance: Floating Income Meets Easing Rates

Ares Capital reported its Q1 2026 results on May 5, 2026, revealing a portfolio that continues to generate robust income, even as short-term benchmark rates have declined.

Key metrics (Q1 2026):

- Net investment income (NII) per share: $0.61 (versus $0.63 in Q4 2025 and $0.65 in Q1 2025)

- Regular quarterly dividend: $0.52 per share (annualized $2.08)

- Supplemental dividend declared for Q1: $0.08 per share (bringing total Q1 payout to $0.60)

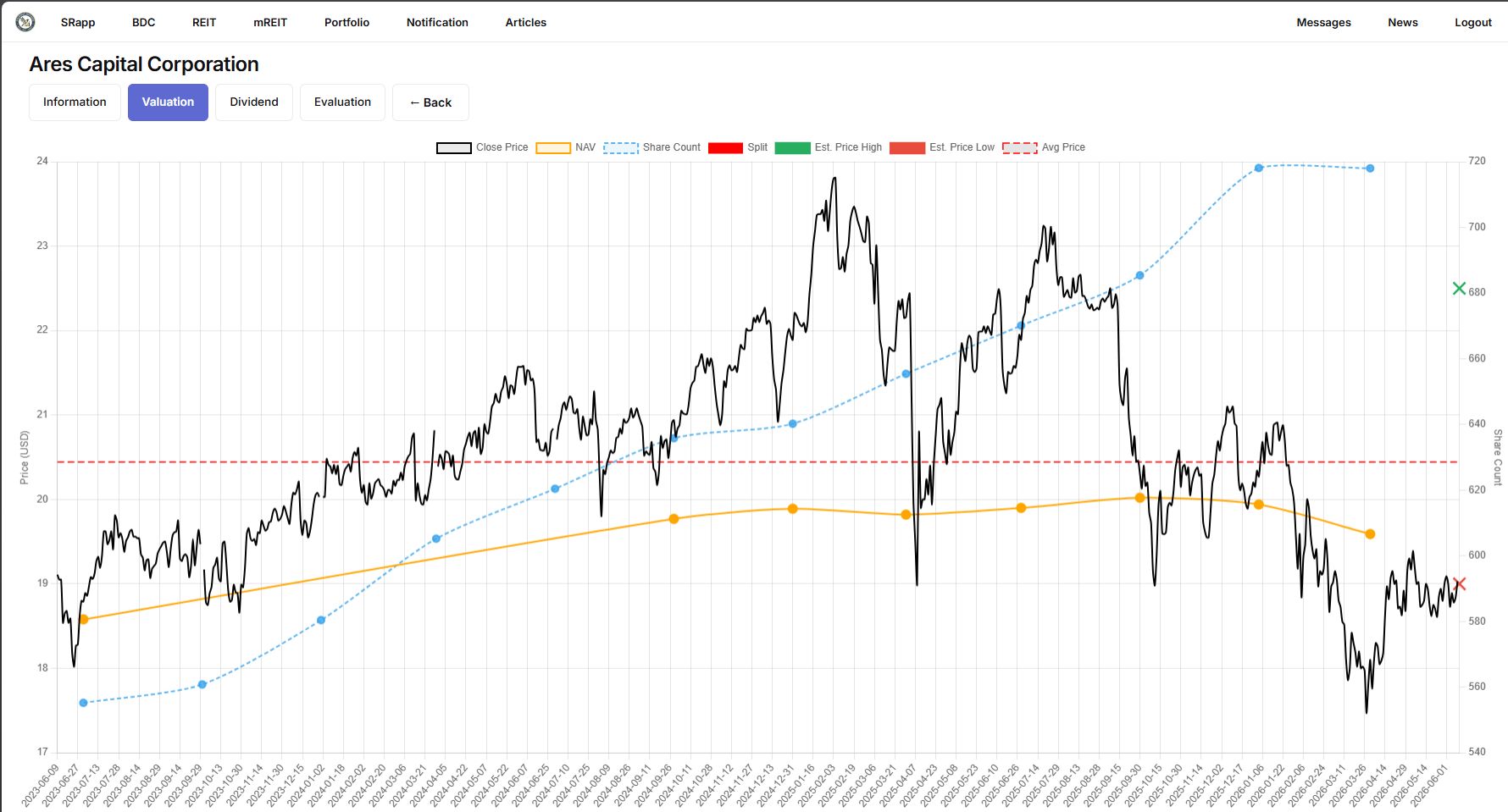

- Net asset value (NAV) per share: $19.85, up from $19.47 a year ago

- Portfolio fair value: $22.1 billion, across 490 portfolio companies

- Weighted average yield on debt investments at amortized cost: 10.6%

- Weighted average yield on income-producing investments at fair value: 9.8%

- Non-accruals at fair value: 1.2% of the portfolio, well below the BDC industry average of 2.4%

The slight decline in NII reflects the passthrough of lower SOFR (Secured Overnight Financing Rate) on the approximately 85% of ARCC’s loan portfolio that carries floating rates. However, the vast majority of these loans have SOFR floors averaging just below 1.5%, which are deeply in the money. More critically, the spread over SOFR that ARCC commands on its directly originated loans has expanded to approximately 600–650 basis points, as middle-market borrowers continue to accept higher pricing in exchange for certainty of execution. This spread expansion has partially offset the 150-basis-point decline in short-term base rates from their 2024 peak.

Balance Sheet & Debt Maturity: Locked-In Financing, Laddered Maturities

A key differentiator between a premium BDC like Ares Capital and a mortgage REIT is the liability structure. ARCC funds its portfolio with a combination of unsecured institutional notes, a revolving credit facility, and CLOs/structured vehicles. Importantly, it has access to long-term, fixed-rate unsecured debt, which it has aggressively locked in.

Credit profile and metrics (Q1 2026):

- Total debt outstanding: $12.4 billion

- Weighted average interest rate on all debt: 4.3%

- Percentage of fixed-rate unsecured notes: 67% of total debt

- Weighted average remaining maturity on unsecured notes: 5.2 years

- Unsecured notes carry investment-grade ratings: BBB / Baa2

- Revolving credit facility commitments: $5.8 billion, with $1.9 billion drawn

- Leverage ratio (net debt/equity): 1.08x (statutory leverage target 1.0x–1.25x, with BDC regulations allowing up to 2.0x)

Unsecured debt maturity schedule (as of Q1 2026):

| Year | Maturities ($B) | % of Total Unsecured Debt |

| 2026 | $0.5 | 6.0% |

| 2027 | $1.11 | 3.3% |

| 2028 | $1.41 | 6.9% |

| 2029 | $1.0 | 12.0% |

| 2030+ | $4.3 | 51.8% |

Only $500 million of unsecured notes mature in the remainder of 2026, and $1.1 billion in 2027—a trivial amount relative to ARCC’s $5.8 billion credit facility capacity and its strong cash flow generation. Moreover, because ARCC issued the bulk of its long-term notes when base rates were higher, the weighted average coupon on its unsecured debt is 4.8%. With the Fed now in an easing posture, the company will have the opportunity to refinance 2027–2028 maturities at potentially lower rates, gradually reducing its interest expense. This is the mirror image of a mortgage REIT: ARCC’s funding costs can decline as the Fed cuts, even as its asset yields compress only gradually.

The interplay between Fed policy and ARCC works through three channels:

- Asset income: A 100-basis-point drop in SOFR reduces annual portfolio interest income by roughly $0.07 per share, partially mitigated by spread expansion and floor protection.

- Liability cost: Unsecured fixed-rate debt is unaffected in the short term; floating-rate debt (revolver and some CLOs, ~33% of total) reaps an immediate benefit.

- Credit quality: Lower base rates reduce the interest burden on the middle-market borrowers themselves, lowering default risk and supporting the value of ARCC’s equity co-investments. Historically, ARCC’s non-accrual rate falls during easing cycles as over-levered borrowers find breathing room.

The net impact of a moderate easing cycle is a mild decrease in NII—which we have already seen—but not a material impairment of dividend coverage.

Dividend Coverage and Sustainability: A Wide Moat Around the Payout

Ares Capital’s dividend architecture includes a fixed regular quarterly payout and a variable supplemental dividend designed to distribute excess earnings. In Q1 2026:

- Regular quarterly dividend: $0.52 per share

- Supplemental dividend: $0.08 per share

- Total Q1 distribution: $0.60

- NII per share: $0.61

- Payout ratio on NII (including supplemental): 98.4%

- Payout ratio on regular dividend alone: 85.2%

For the trailing twelve months, NII per share was $2.46, while total dividends declared were $2.32 ($2.08 regular + $0.24 supplemental), representing a payout ratio of 94% of NII. The regular dividend was covered with an 85% payout ratio, leaving a meaningful cushion of approximately $0.38 per share annually even before considering the supplemental.

This level of coverage is among the strongest in the BDC universe. ARCC also has $0.52 per share of undistributed earnings (spillover income) carried forward from prior years, providing an additional buffer to maintain the regular dividend through a temporary earnings dip. NAV per share has increased steadily over the past year, indicating that the company is not eroding equity to fund the dividend—a critical sign of sustainability.

Furthermore, Ares Capital’s credit machine has proven itself across cycles. The 1.2% non-accrual rate is remarkably low for a middle-market portfolio. The weighted average loan-to-value on its portfolio is 43%, giving substantial equity cushions. And with the direct origination platform of Ares Management behind it, the company can selectively deploy capital at high spreads even in a lower-rate environment.

Risks to Consider

- Continued base-rate cuts: If the Fed slashes rates aggressively—say, below 3%—ARCC’s NII could decline more meaningfully. The loan floors provide a backstop, but spread compression may eventually occur. NII per share could dip toward $0.55, still covering the regular dividend, but supplemental payouts would shrink.

- Spread widening on funding: Although currently a benign risk, if ARCC’s credit rating were downgraded, its unsecured borrowing costs could rise. This is unlikely given the company’s size, scale, and conservative balance-sheet management.

- Middle-market recession: A broad economic downturn could push non-accruals toward 3%–4%, requiring realized losses and a reduction in NAV. ARCC’s strong underwriting and senior-secured focus mean recoveries have historically been high, but losses are possible.

- Competition from private credit: As rates fall, institutional investors may return to syndicated markets, reducing the opportunity set for direct originators like ARCC. However, the middle market remains underserved by banks, and ARCC’s scale gives it a competitive moat.

Conclusion: The Gold Standard Earns Its Keep in All Rate Regimes

Ares Capital is not a bond proxy that withers when the Fed pivots—it is a credit engine that thrives on high underwriting spreads and modest leverage, and its locked-in fixed-rate debt insulates it from the funding volatility that plagues mortgage REITs. The recent decline in base rates has shaved only a few cents from quarterly NII, leaving the regular $0.52 quarterly dividend covered by a comfortable 85% payout ratio. With a strong balance sheet, a diversified $22 billion portfolio of senior-secured loans, and a management team that has delivered double-digit returns on NAV over decades, ARCC’s 9% yield is one of the most sustainable high-income streams available.

For investors seeking durable income that does not depend on interest rate forecasts, Ares Capital remains the BDC blueprint. Dividends may ebb and flow with the supplemental component, but the core payout—and the capital behind it—is designed to withstand exactly the kind of gradual easing cycle we are in today.

Comments (0)

Log in to leave a comment.

No comments yet. Be the first to comment!